Save tax up to ₹75,000 ~ u/s 80D.

Save tax up to ₹75,000 ~ u/s 80D.

Cancer Insurance is a medical cover offering financial and healthcare protection against major cancer-related treatment expenses at all stages. The policy offers lifelong-renewability and wide sum insured options.

View MoreReasons to Choose Care Health Insurance?

A cancer insurance policy is a financial cover that lowers the burden of cancer treatment with coverage for hospitalisation, therapies, and other non-medical expenses. It is a financial safety net that helps people during unprecedented cancer detection. The cancer insurance plan offers complete protection from pre-hospitalization tests to patient care and post-hospitalization treatments. This way, people across ages can secure their health and savings against the life-threatening cancer disease accounting for over 10 million deaths in 2020.

Every year, over ten lakh people are diagnosed with cancer in India, and another six to seven lakh people lose life to this life-threatening condition. Studies anticipate that India might witness over 17 lakh new cancer patients by 2035 and 12 lakh deaths yearly. The alarming facts and unprecedented health conditions are the major reasons you should opt for cancer coverage. Further, the coverage of family health insurance plans might prove to be insufficient to cover the expensive treatment costs of specialised cancer treatment. Other critical reasons to buy a cancer insurance plan are:

Increasing Cancer Cases

Cancer is the leading cause of death worldwide– pointing to the need of early detection and timely treatment and care

Expensive Treatment Cost

Treatment cost of cancer goes in lakhs and sometimes beyond; thus you need suitable coverage & security for a lifetime.

High Risk of Ailments

Old age people are most vulnerable to the risk of cancer due to age-related ailments and weaknesses, that must be covered.

Financial Struggles

Cancer is a terrifying condition that pushes people into the financial and emotional turmoil that can be avoided with a mediclaim plan.

Family History of Cancer

If you have a family history of chronic or heavy chain diseases, you should opt for a plan covering several cancer conditions.

Cancer insurance works on the same indemnity principle as other health plans, with a fixed sum insured for a payout of regular premium amounts. One can buy a cancer cover individually for a tenure of 1, 2, or 3 years.

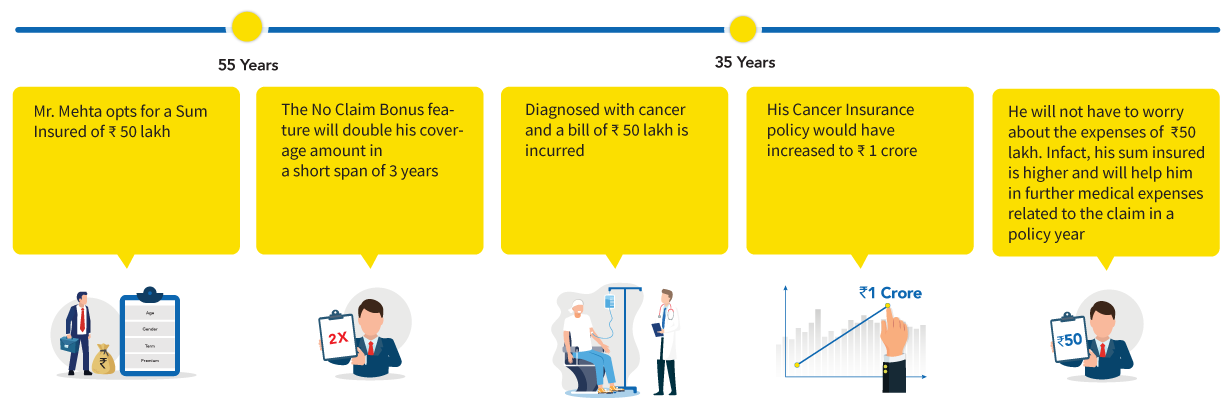

The foremost step is to determine how much coverage suits you based on your health status and budget. Once you choose an adequate sum insured, you can file for a cancer-related claim after completing the required waiting period of initial 90 days and 2 years for pre-existing diseases. Also, you can pay the premium in easy instalments in a monthly or quarterly mode. Note that your sum insured is bound to increase by a maximum of 50% as a reward for staying healthy and maintaining a claim-free year. Learn more about how cancer insurance works with the help of the below example.

People below 50 are eligible to secure their lives with a Cancer Insurance Plan by Care Health Insurance. Here are some other crucial cancer policy details:

| Cancer Insurance Plan Details | |

|---|---|

| Minimum Entry Age |

|

| Maximum Entry Age | 50 Years |

| Exit Age | No Bar |

| Cover Type | Maximum 6 Persons on Individual Basis |

| Tenure | 1/2/3 Years |

| Pre-policy Medical Check-ups | No Medicals Required |

| Sum Insured Options | 10 Lakhs to 2 Crores |

An unhealthy lifestyle, physical inactivity, smoking, and drinking are the major causes of cancer. That’s why you need complete protection against the health risks arising due to cancer. Check out the wide-ranging coverage and benefits of the cancer cover policy by Care Health Insurance:

With adequate coverage and unique benefits, a cancer insurance plan offers the right security against financial crunches. However, before you buy a plan, it is essential to read the policy documents thoroughly and be informed about the following exclusions:

Some of the best cancer care plans in India provide a 15-day Free Look Cancellation period, allowing prospective policyholders to review the policy's terms and conditions before committing to it. If you find them unsatisfactory, you can return the policy documents, expressing dissatisfaction which will allow for a refund of the premium charged, as per the terms and conditions of the policy.

Cover for Treatment of Cancer at all Stages

Health Insurance Coverage for 32 Critical Illnesses

Health Insurance Covering 16 Major Health Aliments

Coverage for wide array of defined surgeries

Filing a claim under cancer insurance is similar to filing a claim under your standard health plan. At Care Health Insurance, our in-house claims department ensures that your claim requests are addressed and processed with the given TAT while promising a seamless process. You can easily raise a cashless or reimbursement claim by following these steps:

Please note, you must inform our claims team within 24 hours in case of emergency hospitalisation and 48 hours prior to any planned hospitalisation.

| Cashless Claim Process | Reimbursement Claim Process |

|---|---|

| Step 1: Go to a listed in-network hospital. Step 2: Fill out the proper forms at the insurance desk. Step 3: Send the completed form to our claim management team. Step 4: When your claim is verified, you'll get an approval letter. Step 5: Respond to queries from the claim management team. You will get information as soon as your claim gets approved or rejected within the standard TAT. |

Step 1: Submit your claim form and other required documents. Step 2: When your claim is verified, you'll get an approval letter. Step 3: Respond to queries raised by the claim management team. Step 4: Get approval from the claim management team. Step 5: Our claims team will contact you if there are specific reasons for rejecting your claim. |

Care’s cancer mediclaim is one of the most promising cancer care insurances that ensure its support when you are most vulnerable. Cancer is a dreaded disease that requires attention and constant care. We believe in providing a safety cushion that ensures smooth recovery beyond the post-hospitalisation period. Care Health Insurance’s cancer health insurance covers all types of cancer, including-

Care’s cancer policy comes with comprehensive benefits that would help you when you need financial assistance during your treatment of any kind of cancer.

Cancer care plans and healthcare policy work on the same principles of indemnity yet differ with respect to coverage, sum insured options, and eligibility. Also, you may be insured under a standard health cover but would still need a separate cancer insurance plan to ensure protection against cancer-related medical expenses. Here, read about the major differences between the two plans:

| Factors | Cancer Insurance | Health Insurance |

|---|---|---|

| Coverage | A comprehensive cancer care policy covers all incurred medical expenses related to cancer. | Covers the general medical and surgical costs of the insured person. Hospital costs are covered and there may be sub-limits for room rent, etc. |

| Who Should Buy? | Individuals who have higher risks should consider the cancer care plan. In addition to a basic policy, you can buy a cancer care policy to supplement the protection. | A standard health policy should be purchased by everyone, regardless of age. With rising healthcare prices, health insurance should take priority in your financial plan. |

| Why Should You Buy? | A regular health plan could be insufficient in the event of a serious illness or cancer. As a result, critical illness and cancer coverage are needed.It covers the cancer care expenses incurred that can be otherwise financially challenging. Also, the compensation under cancer insurance plan can be used to pay off the other financial liabilities. | It is a simple indemnity-based plan that reimburses medical costs or provides cashless health care. It is ideal for covering rising hospitalisation costs, care, diagnosis, medical assistance, and other medical expenses, thus enabling one to bear the impact of medical inflation. |

It is important to purchase a comprehensive cancer care plan, such as the one provided by Care Health Insurance. Cancer insurance outperforms most healthcare plans because the cost is low and coverage is available for all stages of cancer.

Below are the main benefits of purchasing your insurance for cancer treatment online:

If you are anxious about your maternity, we have maternity insurance taking care of your precious journey.

Buying an ideal cancer policy in India can be confusing, especially when you are unaware of the types and extent of expenses incurred toward cancer treatment. While choosing suitable insurance for cancer patients, here are the crucial things that you should consider:

Once you have chosen the right cancer insurance plan for yourself or a family member, you can buy the policy online in the following steps:

Step 1

Generate the quote for Cancer Insurance by visiting Care Health Insurance’s official website.

Step 2

Fill in the information about insured members, their age, health condition, and gender.

Step 3

Customize your policy by selecting a suitable sum insured, policy period, and premium payment options.

Step 4

Pay the premium using any safe digital payment method, like net banking, debit or credit cards.

Once approved, you will receive the policy documents at your registered e-mail address, including the e-health card.

Look for hospitals around you

My appreciation for your prompt service

Rahul Sangwan

Health Insurance

We will continue to avail of your scheme

Samanway Barik

Health Insurance

Everything went very smooth

Soubhagya K Kulkarni

Health Insurance

Really helpful explaining the process in advance

Vaibhav Rai

Health Insurance

Zeroing in on a health insurance plan for your family is a tricky choice, given the number of insurers in the market who offer similar policies. It is not wise to simply choose the policy with the lowest amount of premium. You need to compare different policies, their features and benefits. Care Health Insurance (CHI) is a specialist Health Insurer and offers products keeping in mind the needs of a customer in the event of a medical exigency. CHI offers a distinct set of benefits giving a clear choice for providing you with the best possible health insurance.

Best Health Insurance

Company of the

Year*

48 Lakh + Claims Settled**

24800+

CASHLESS HEALTHCARE PROVIDERS^^

Yes, you would need separate cancer insurance since your basic medical policy may not cover the treatment cost of cancer. There will always be limitations in a standard health plan, which may not allow you to avail of the treatment that caters you complete coverage of your cancer treatment.

Yes, you will be entitled to a maximum of 50% no-claim bonus throughout the cancer treatment policy tenure as a reward for not requesting any claims.

Our cancer care policy is an indemnity-based health plan. We will cover the actual medical costs you incur during your cancer care within the policy period on a reimbursement or cashless basis, subject to policy terms and conditions.

Our cancer insurance plan offers sum insured options ranging from Rs 10 lakh to Rs 2 crore. You can enhance the coverage with optional benefits like unlimited automatic recharge, air ambulance coverage, and room rent modification at an additional premium, thus enhancing your health coverage.

The reimbursement process under our insurance plan for cancer is easy and quick. Our in-house claims management team will address and process your claim within 15 days of receiving your request. Also, the team will keep well-informed about any discrepancies in the documents submitted. The final claim is settled or denied (as per the policy terms) within 30 days of receiving all the documents.

No, a medical check-up is not mandatory before purchasing insurance for cancer coverage. However, policyholders may need to undergo a few examinations depending on their health status and at the underwriter’s discretion.

According to Section 80D of the Income Tax Act of 1961, an individual who purchases cancer mediclaim is entitled to receive an income tax deduction on the premium charged for it. These tax advantages are subject to changes in the tax laws in India.

When choosing the best cancer care policy, you should choose a sum insured that is large enough to cover the different medical expenses you will face in the future. It will cover hospital costs, medical tests, and medicines, among other things.

You cannot opt for cancer insurance or mediclaim for existing cancer patients. To opt for a cancer plan, you should check the policy eligibility and disclose your medical history honestly.

Cancer insurance costs depend on several factors like the sum insured, your age, optional benefits, etc. Before purchasing a cancer insurance plan, review the policy benefits, waiting period, and entry age, and check the applicable premium.

If you cannot pay the premium for your cancer insurance policy on the due date, a grace period of up to 15 days will be allowed depending on the policy terms. During this grace period, you can pay the premium for your cancer care policy without any penalties. However, if you fail to pay the premium after the grace period has ended, it will lead to a policy lapse.

The cancer insurance plan offers lifetime renewal option to the policyholders. You can renew the policy online in a few easy steps. Access Care Health Insurance official website and go to the renew section. Enter complete details and make premium payment through any secure payment mode.

You will have a grace period, which is generally 30 days from the policy's expiration date, to renew the cancer cover plan, subject to the policy terms and conditions.

The coverage for different stages of cancer depends on the cancer insurance plan. It can vary depending on the extent of healthcare required to treat the condition.

Yes, you can buy cancer insurance for your family members, either by adding them to your policy on an individual basis or by purchasing a standalone policy for them. Refer to the terms and conditions of your chosen plan with cancer cover for more details.

It is not possible to get cancer insurance for pre-existing cancer patients.

As the cost of medical treatment is at an all-time high and only expected to increase in the coming future, it is best to opt for a higher sum insured. You should carefully assess your financial profile and health history before arriving at the adequate sum insured for the cancer insurance. Generally, anywhere 50 lakhs above is a favourable amount for a cancer insurance plan.

Disclaimer: Information above is just for reference. Kindly read T & C of policy thoroughly, Do refer IRDAI guidelines for tax exemption conditions.

Underwriting of claims for cancer is subject to policy terms and conditions

#Premium starts @₹9/day for an 18-year old individual for a policy tenure of 2-years. Overall premium may vary for different individuals.

*Sum Insured – Rs.50 Lakhs, Age – 18 to 25 years, Monthly Premium Payment Mode including Optional covers included - Room rent modification/ Air ambulance cover/ ISO. Exl GST.

~Tax benefit is subject to changes in tax laws. Standard T&C Apply

**Number of Claims Settled as of 31st March 2024

^10% discount is applicable for a 3-year policy

^^Number of Cashless Healthcare Providers as of 31st March 2024

Get the best financial security with Care Health Insurance!

Sales:phone_in_talk1800-102-4499

Services:![]() 8860402452

8860402452

Buy Now

Live Chat

Terms & Conditions of Premium Quote Generation

"Care Health Insurance Ltd & associate partners may contact you to assist you with website navigation of www.careinsurance.com and assist in proposal filling."